It’s been said that “numbers never lie.” So while we may feel like our day-to-day work keeps our finger on the pulse of the Northern California commercial real estate market, it’s always good to look at the numbers and see what’s real.

So every month we scour the data in each of the regions NAI Northern California covers and determine the health of our primary markets in office, retail, industrial and multifamily properties. We check four indicators in each asset class:

- Current Inventory

- Under Construction

- 12-Month Net Absorption

- Vacancy Rate

Here below is our November 2019 report for San Francisco, which we’ve also compiled into an eye-friendly infographic. Follow our blog, social media feeds, or subscribe to our newsletter for monthly updates to this data, and for our companion reports on the East Bay, North Bay, and South Bay.

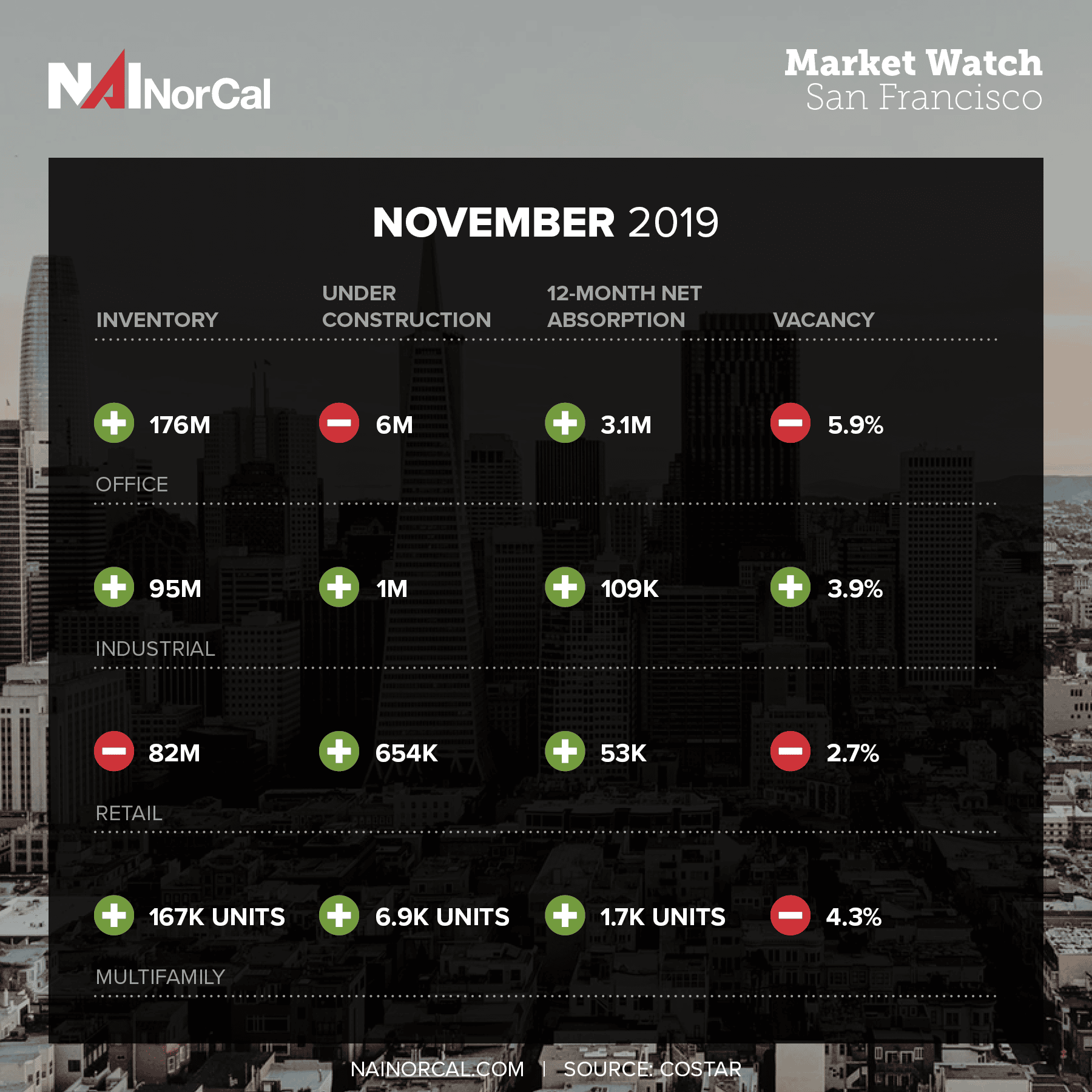

The Data

Office Properties: This month, the San Francisco office market’s inventory is just slightly up from October, at 171 million sq. ft., with 6.3 million additional sq. ft. under construction. This figure is up about 300,000 sq. ft. from last month but is expected to decline. Twelve-month net absorption stands at 2.8 million sq. ft. of office space, which is down about 200,000 from last month. The vacancy rate is barely up this month, at 6.0%, but projected to decrease as the holidays bring limited movement.

Retail Properties: There are 82 million sq. ft. of retail space available in San Francisco, which is the same as the last few months. However, this figure is still expected to drop. More is coming, with about 704,000 sq. ft. under construction (slightly up from October), and the 12-month absorption rate is at at -190,000 sq. ft., which is much lower than in September or October’s positive numbers. Vacancy rates are slightly up from last month but are expected to decline, at 2.8%.

Industrial Properties: For the industrial market, 94.5 million sq. ft. of space is in the inventory, just up from last month, and this number is expected to continue to rise as the 2.4 million sq. ft. currently under construction wends its way towards completion. Construction is expected to increase, though likely slowly given recent trends and the approach of the rainy season. The 12-month net absorption rate is at -27,700 sq. ft., shockingly down compared to September and October’s positive numbers, and the vacancy rate is at 3.9% and holding steady.

Multifamily Properties: The multifamily market is very slightly down from last month, with up to 166,000 units available in the inventory. Construction is also slightly down from last month, at 6,762 units, but projected to increase despite the season. The 12-month net absorption rate continues to slowly decline, at 1,605 units for November. The vacancy rate is 4.7%, which is higher than the last two month, but is projected to drop.

For more detailed updates or to find out how San Francisco’s submarkets are doing, contact one of our advisors. Whether you’re interested in office, industrial, retail, or multifamily properties, we can help.

Data source: Costar Analytics

{kind=link}